WASHINGTON — The Surface Transportation Board today issued a setback to Union Pacific’s effort to acquire Norfolk Southern, rejecting the railroads’ merger application as incomplete — although that move offers little clue to the eventual prospects for the first transcontinental merger.

The decision will slow the merger process, requiring the two railroads to rework three areas where the board found fault with the original 6,692-page application filed in December. UP and NS have until June to submit a revised application, but are not expected to need that long.

The board said in its 15-page decision that it rejected the application based on problems with market-share data, the failure to include the complete merger agreement between the two railroads, and how the application addressed control of the Terminal Railroad Association of St. Louis.

To the first point, the board found a disconnect between the application’s projections of extensive growth and its use of 2023 data to define the market share that would be controlled by the merged railroads. “The application does not contain future market share projections showing the combined effects of merger-related growth, diversions, and merger-influenced and other changes to market conditions that Applicants anticipate,” the board said in a press release. “Today’s decision finds that Applicants’ market impact analyses must necessarily project market shares beyond the transaction’s consummation date, and therefore that the application does not include the ‘projected market shares’ as required,” the release says.

The board also agreed with the contention made by other railroads that the application was incomplete because it did not include all of the merger agreement between UP and NS, omitting a section on terms that would allow UP to walk away from the transaction. The lack of that information means the application does not, as required, contain all “contract[s] or other written instrument[s] … pertaining to the proposed transaction,” the board found, and also did not justify the decision to withhold that information.

Finally, the UP-NS application treated the disposition of the TRRA as a minor transaction, but the board ruled it is a significant transaction, which in itself requires a more detailed application. Because the application regarding the TRRA is incomplete, the larger UP-NS application is also, the board said.

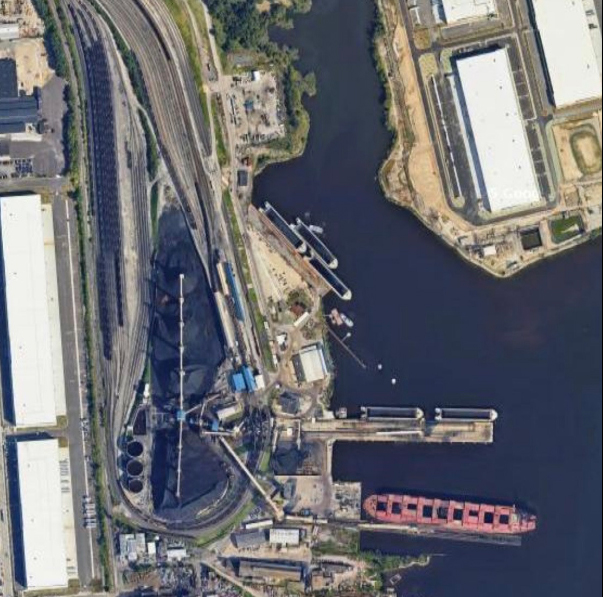

The TRRA is jointly owned by UP, NS, BNSF Railway, Canadian National, and CSX. The merger would give UP a controlling interest, although the merger application says UP plans to divest the share that would give it control. The TRRA application connected to the UP-NS deal addresses control if divestiture cannot be completed by the time the UP-NS deal is consummated.

The board noted that commenters had argued that the application was incomplete in other ways, but said it would not reject the application on those grounds, but reiterated that “should the applicants choose to file a revised application, nothing prevents Applicants from making additional changes to improve their Application now that they have received comments from other stakeholders.”

The board said in its press release that today’s decision “should not be read as an indication of how the Board might ultimately assess any future revised application.”

And there is recent precedent for rejection of an application that was ultimately approved. The initial CSX application to acquire Pan Am Railways was rejected for lacking all necessary market analysis [see “Federal regulators reject CSX-Pan Am merger application …,” Trains.com, May 26, 2021.] An updated application was filed three months later and accepted by the STB; the board went on to approve that application in April 2022 [see “Regulators approve CSX Transportation’s acquisition …,” April 14, 2022].

UP and NS have until Feb. 17 to inform the board if they will file an updated application, and until June 22 to complete that filing. An analyst note from financial services company Baird estimated this week an updated application could take 30 to 90 days to complete.

Union Pacific’s response to the decision was terse: “Union Pacific will provide the additional information requested by the Surface Transportation Board.”

Other Class I railroads welcomed the news.

The longest comment came from Canadian National, which this week asked the STB to compel UP and NS provide more information. CN said the board had “rightly” rejected the application.

“Simply put this application is missing the last mile,” CN said. “This decision reinforces that a merger of this scale cannot be assessed on omissions or partial disclosure and must be evaluated on a full and transparent record, as required by the heightened standards under the new merger rules. …

“As noted earlier, applicants had refused information critical to understand their perspectives on anticipated competitive harms and inform the Board’s public-interest and competitive analyses. The Board rightly found that applicants needed to provide that information.”

BNSF Railway said it applauded the STB decision “based on the application lacking core information critical to determining the proposed merger’s impact on competition. We also appreciate the STB’s willingness to consider the views of all stakeholders as part of the regulatory review process.”

CSX said similarly, “We appreciate the Surface Transportation Board’s thorough review and consideration of public and stakeholder input. We will continue to actively participate in the STB’s review process to ensure CSX remains well-positioned to compete, reinvest in our network, and deliver best-in-class service for our customers.”

CPKC had the briefest response: “Today’s decision clearly demonstrates what we have believed from the beginning, that the Surface Transportation Board will thoroughly review and carefully consider this proposal.”

— Revised and updated throughout at 6:08 p.m. CT. To report news or errors, contact trainsnewswire@firecrown.com.

I know this is a small potatoes issue, but I do believe it needs to be addressed in regards to future route expansion of Amtrak routes-how will this acquisition affect the potential routes through Louisiana via the Meridian Speedway and possibly between Baton Rouge and New Orleans? NS and KCS spent a lot of money on the Speedway deal and I’m pretty sure NS (and UP) still would resist Amtrak stepping into their territory. Will the expansion aspect be protected?

STB approval needs to have a requirement that UP will not have any service delays more than what is occurring now. That especially means Amtrak and all freight customers.

That should be a requirement for every road whether the merger happens or not. But no one can see the future so there needs to be a “circuit breaker:” clause, but not one that is easily used, like embargoes were until the STB redefined them and put teeth into there regulatory enforcement. Amtrak, however, needs to prove it can run its own house before it can demand anything.

Sorry Union Pacific you do not have all your data so this merger is rejected!

Union Pacific went into merger court without its paperwork You know what happened the last time they did that they killed the Rock Island and the Milwaukee Road and Surface Transportation Board wants to make sure that they don’t make the same mistake twice.

If you want to merge you must have all your paperwork. Canadian Pacific and KCS submitted their paperwork on time and all the data was there and Surface Transportation Board for both Canada and the United States said yes.

This is not Wall Street. You do not do a merger through pump and dump You need all of your data. If you do not have that data and you go into merger court they are going to say no, They’re going to reject it, your application will be sent back to you, your feasibility study will be denied, and you will have to start from square one.

Union Pacific Norfolk Southern you guys have 30 days to get that data or the answer is No.

Not sure where you’re getting a “feasibility study” out of this. Also, Union Pacific had next to nothing to do with the Milwaukee Road dying, that was their own fault.

Union Pacific has until February 17th to say if they want to refile. They have until June 22nd to do so. That’s a lot longer than 30 days.

Or the Rock Island… blame that on the Interstate Commerce Commission for taking EIGHT YEARS to make a decision to save a dying railroad that wasn’t worth a plug nickel when they FINALLY did make a decision.

I don’t mean to sound like an old-time beauty contest winner who only wanted world peace and a pony, but I’d really like to see a merger proposal that actually helped shippers, that didn’t hurt employees or communities, and that flipped the bird to stock market analysts and vulture investors.

While I’m having that pie in the sky outlook, I’d like to see a Class One line that didn’t treat employees and customers like a necessary evil that they can barely tolerate.

Why not just rule that the UP-NS merger cannot be consummated until UP divests itself of at least 1/7 of TRRA? If they want the deal bad enough they’ll find a way to make it happen. UP owns 3 shares; NS, CSX, CN, and BNSF hold one share each.

Read the story, They said they would divest the offending shares (two) to make the deal work but they aren’t going to do that without being granted the purchase agreement, That would hurt both UP and NS.

“The TRRA is jointly owned by UP, NS, BNSF Railway, Canadian National, and CSX. The merger would give UP a controlling interest, although the merger application says UP plans to divest the share that would give it control. The TRRA application connected to the UP-NS deal addresses control if divestiture cannot be completed by the time the UP-NS deal is consummated.”

UP already has 100% control of the Alton & Southern.. It should be required to divest all shares in TRRA..

Alton & Southern is solely in Illinois. TRRA has the two bridges over the Mississippi: MacArthur and Merchants. UP has to keep an ownership share in TRRA to cross the river.

this merger is solely driven by Wall st. it definitely will not take trucks off the road and most likely add trucks as already poor service by all class 1 railroads continues. class 1s don’t know anything about service, all they know is Wall st. I hope the board realizes this.

I’m very happy that the STB is at least going to make them work hard for it. Let’s see what they got! I think it is bound to happen. Follow the history of the industry. Next step after this is perhaps Nationalization. Well, at least the real estate. The Shortlines could send their products directly to their customer’s siding, and vise versa. Would that work?

I don’t have any direct experience with these types of applications. My comments are based solely on the article above. I’m amused that this application of 6,692-pages is incomplete! It will be interesting to see how many more pages get added.

Why nationalize an industry that is successful, at least at the macroeconomic level. Nationalization GUARANTEES losses and an inability to innovate (why do you think Europe still uses something as archaic and chain and buffer couplings?) The Class Ones must certainly increase their service levels to justify their common carrier status, and UP is already experimenting with this with their moves (ironically) in Oregon, the most socialist state in the US.

BAM! Finally an independent government agency not being influenced by politicians. While I see the good and bad on the acquisition (this is not a merger). My big concern is how they will treat smaller shippers. They already blow off customers not having a large enough load to move. Small shippers call and often times do not even receive a call back. Not what I would consider even average customer service. All of the big boys are guilty. They focus on lower margin unit trains not manifest freight. Margins on manifest freight are higher. The acquisition will not take a measurable amount of trucks off the road. For shippers that is their only alternative to ship their goods. As long as wall street (here’s looking at you Ancora) runs the show nothing will change. Dividends to shareholders just good business to reward the investors, however buying back stock in lieu of reinvesting in the business is mind blowing. No wonder the industry does not grow.

Surface Transportation board for Canada and the US said yes for KCS and CP Rail because they had their data and Keith Kreel is not a robber baron like the person who is running Union Pacific. If you are going to run a railroad you need a railroader at the home. When Wall Street gets involved it is pump and dump and that’s how you lose mergers. They need all their paperwork or the answer is No.

Aaron the Transportation Board of Canada is IRREVELANT. This is a US Transaction. The STB granted (Wrongly by most railroads opinion, especially CN) that the CP-KCS Merger was under the old, less stringent rules than this merger. This merger is breaking new ground. And with new ground comes new expectations. Sad to say, any other future mergers will have the benefits of knowing what is expected, volume wise, thanks to the documentary gymnastics that the STB is requiring from UP, the purchaser in this transaction.