Analysts widely expect that BNSF Railway and CSX will seek to merge in the wake of last month’s announcement that rivals Union Pacific and Norfolk Southern would combine in an $85 billion deal to create the first U.S. transcontinental railroad.

“The question around BNSF remains not if but when they will announce a deal to merge with CSX,” Bascome Majors, an analyst with Susquehanna Financial Group, wrote in a note to clients.

BNSF’s corporate parent, Berkshire Hathaway, is sitting on a nearly $350 billion cash stockpile. CSX, meanwhile, reportedly has engaged Goldman Sachs to advise it on merger matters. Both railroads have declined to comment. And there’s no telling when the other merger shoe might drop.

But if the Surface Transportation Board ultimately approves UP+NS and BNSF+CSX — an outcome that is far from certain — it would create two relatively balanced coast-to-coast systems.

How would the two transcontinental railroads compare?

![]()

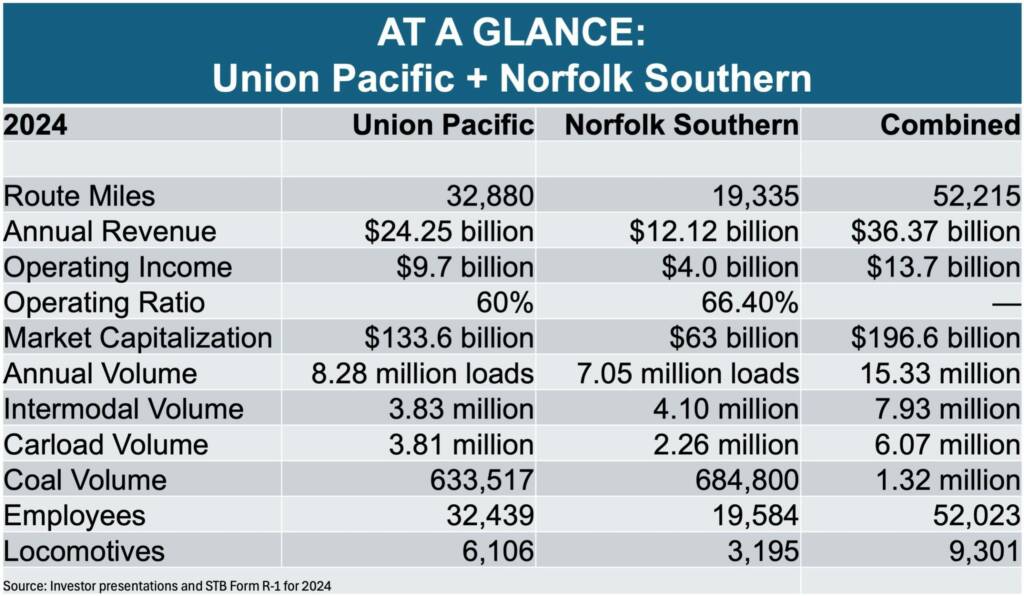

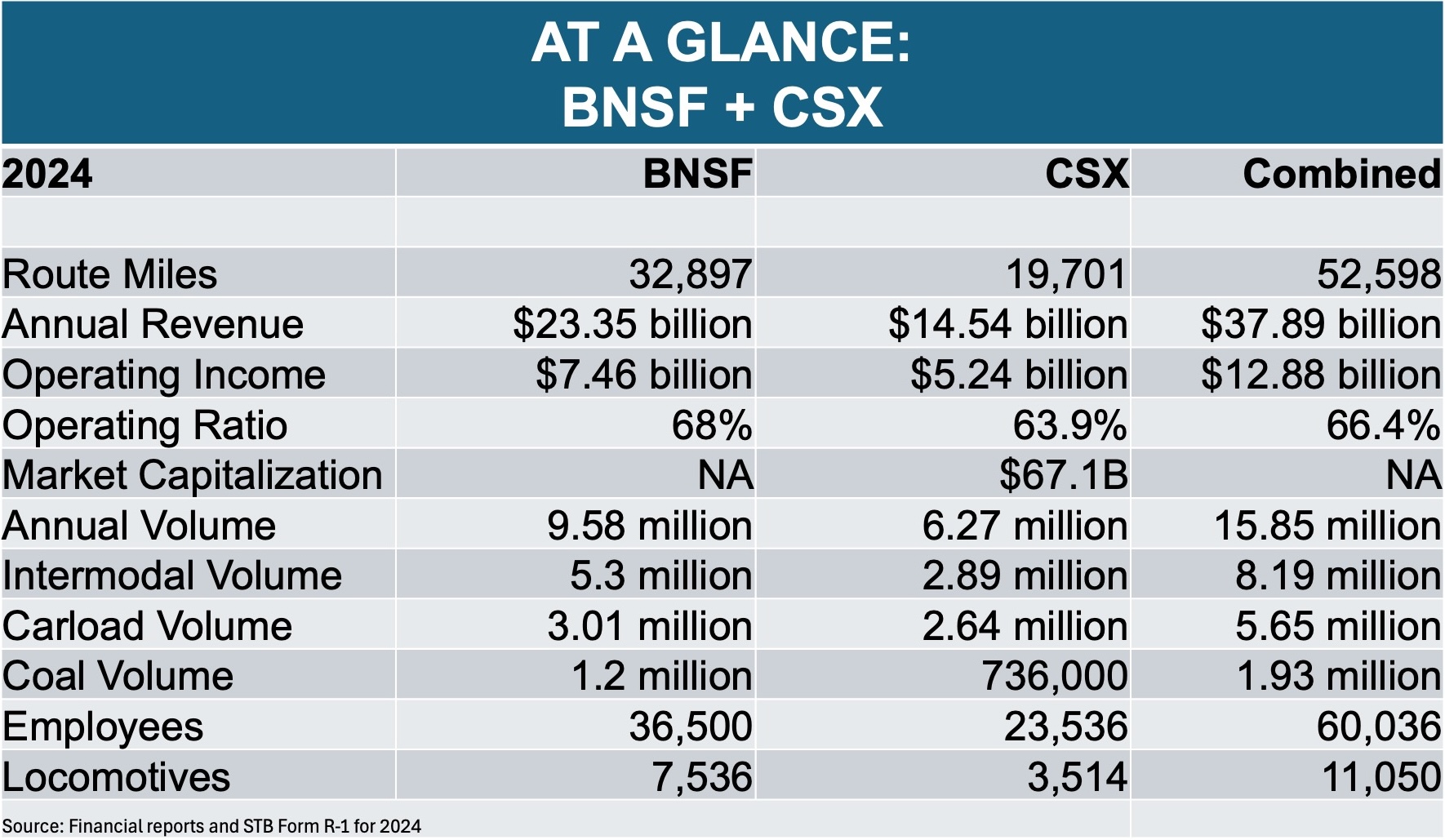

Measured by route miles, the systems are essentially tied at just over 52,000 miles. BNSF+CSX would be ever so slightly larger, with 0.7% more route miles.

BNSF+CSX would have 4% more revenue, based on 2024 financial results. But UP+NS would be more profitable, generating 6% higher operating income and producing a 4.3-point lower operating ratio.

BNSF+CSX also would handle more volume, including intermodal and coal traffic. UP+NS would have a larger carload network.

But the volume difference, based on 2024 data, is not huge: BNSF+CSX would hold a 3% edge over UP+NS.

BNSF+CSX also would have more employees and a larger locomotive fleet, based on 2024 data reported to the STB.

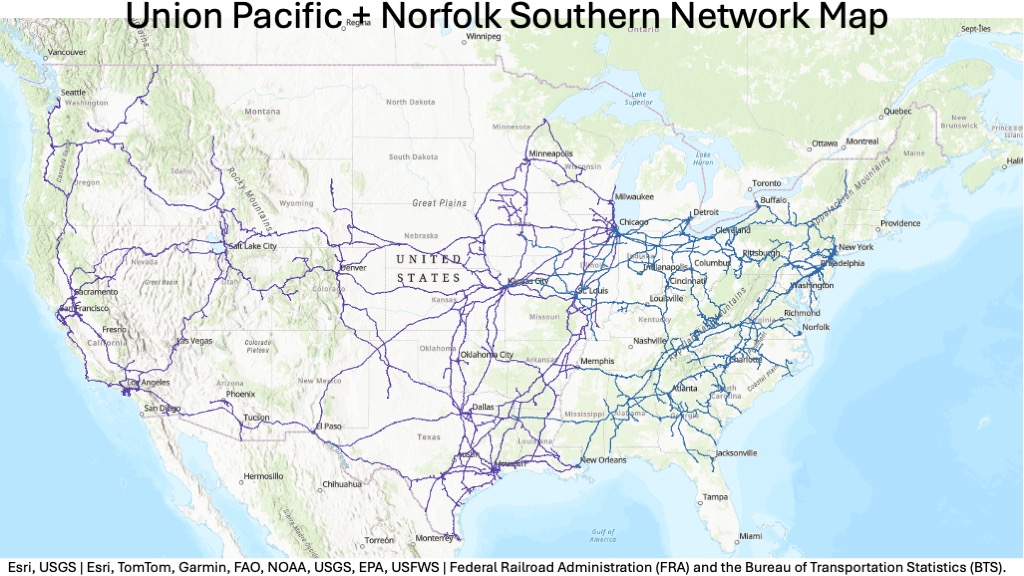

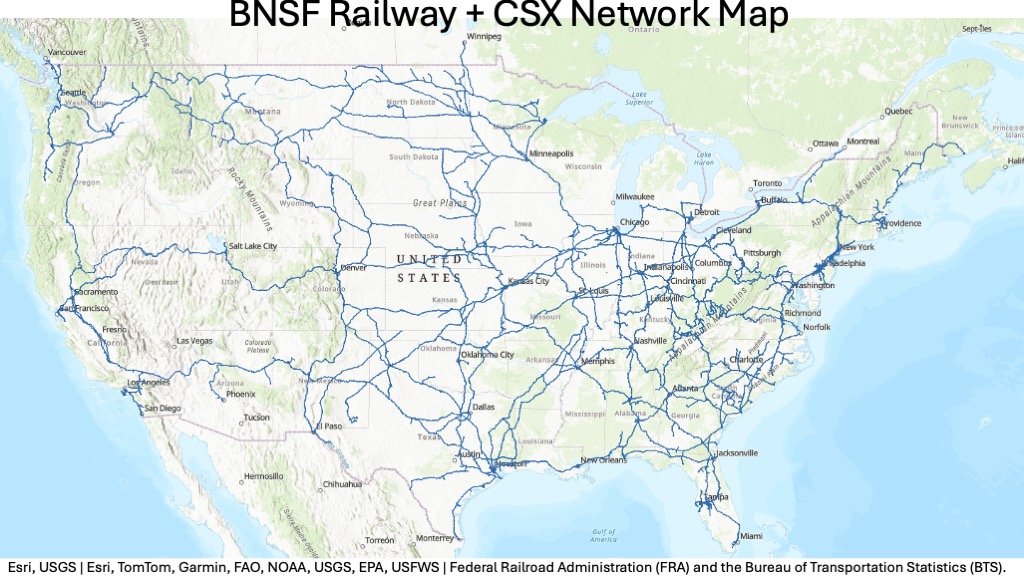

Geographically, the transcontinental tie-ups would still have the same holes in their maps as the current systems — unless regulators condition approval upon plans to fill the gaps in each network.

UP+NS would be absent from the Dakotas and have just a small presence in Montana, Florida, and New England.

BNSF+CSX would still have to rely on BNSF’s sparingly used trackage rights over UP in the Central Corridor that links Denver with Northern California, as well as the direct UP routes linking Houston with Memphis and St. Louis.

Share this article